"The more I find out, the less I know."

|

Weather at the Frozen North

This is my personal blog. My professional blog is The Customer Service Survey I've written a book called Gourmet Customer Service. You can buy it on Amazon. (in)Frequently Asked Questions AIM Screen Name: DFNfrozenNorth

Categories

Statistics

Last Updated: Nov 11, 2008 12:27 PM

|

Tuesday - November 11, 2008 11:55 AMThe DorkmobileInspired by a combination of high gas prices and a desire to get more consistent exercise, this summer I bought a recumbent tricycle and cargo trailer for my commute to work.

Since June, my goal has been to ride to work at least two or three times every week, about a 16.5 mile round trip. I'm pleased to say that I've put over 900 miles on the trike so far (including a few longer rides for fun), and I've saved about two tanks of gas in the minivan. I'm not going to pay for the fancy trike through gas savings alone--at least not this decade--but I've found that riding to work has a number of side-benefits aside from the obvious health and environmental ones. The biggest is that riding the trike is straight-out fun. More fun than driving a car, naturally, but also more fun than riding a bike. The recumbent seat position is much more comfortable than a bike seat (which hurts my butt, and also puts a lot of pressure on my wrists and shoulders), and the low-to-the-ground arrangement gives a palpable feeling of speed like riding a go-kart. I've also found that the trike gets a lot more reaction from other people. Where a bicycle is common and even a nuisance to some drivers, the trike with trailer is a real novelty. I get lots of kids who wave at me as I zoom by, and cars give me a lot of space (and often wave, too). Now that winter is setting in, you might think that riding season is over. Not if I can help it! Within the next week or so, I should be receiving a velokit, basically a tent with windshield for the trike, allowing me to continue riding even on cold mornings. With a trike, slippery roads are not nearly the problem that they are on a bicycle (you can't wipe out on an icy patch). At the same time I'm doing some upgrades of the drivetrain, switching to all-internal hubs (where the gears are inside the wheel, keeping them from being exposed to rain, snow, sand, etc.). Combined with the velokit, The Dorkmobile will be complete, letting me ride in all but the worst winter weather in comfort and looking like a total geek. Posted at 11:55 AM | Permalink | Tuesday - September 23, 2008 07:35 PMWall Street BailoutWhat an amazing couple of weeks. It looks like right now we may be in the middle of the climax of the financial mess which has been building for the past 18 months. At least I hope this is the climax: if there's another act to follow, it will be a doozy. On the other hand, I've been saying since the beginning of the year that I thought we were at or close to the bottom. Foolish me. What scriptwriter can resist the natural drama of a $700 billion bailout of the financial system juxtaposed with what was going to be a historic election anyway? I have a bad feeling, though, that when the inevitable movie versions are made my reaction will be the same as often happens when my favorite books are put up on the big screen: "It was OK, but the original was better written." There's been considerable media coverage and analysis, but not every question has been answered. Here's a little bit of my own analysis: What Happened? The regulations are designed to help in bad times by ensuring that most banks have enough money to weather most storms. In good times, of course, bank failure isn't so much of an issue. Over time, however, more and more of the financial system has migrated from the regulated banking world to the unregulated world of money market mutual funds, commercial paper, hedge funds, CDO's, and so forth. That's because it's easier to make money on the unregulated side (no pesky regulations, after all). To feed the appetite for more investment, higher returns, and greater fees, the unregulated side gobbled up more and more of the financial acitivity which used to be handled by regulated banks. If you're a consumer in the U.S., chances are that at least some of the money you owed to someone was bought, repackaged, sliced, sold, repackaged, etc. Not just mortgages, but credit card payments, student loans, auto loans, etc. all got fed into the machine. Investors and bankers made so much money so fast that the demand for these investment vehcles was nearly insatiable. It helped that the economy was doing great, and default rates were at historically low levels. Because of that demand, it became really easy to borrow money for almost anything, on almost any terms. That easy credit masked the fact that the value of the collateral (the mortgaged house) was perhaps not as solid as everyone assumed. When the party ended and default rates started going up, the value of all these investment vehicles inevitably started to drop. In a normal recession, that wouldn't be such a problem, since banks are required to have enough reserves to buffer against a certain level of defaults from the people they loaned money to. Two things are different this time: first, many of the loans this time around are held by unregulated institutions, whcih are not legally required to hold any particular cushion. The hedge funds and investment banks which own all these slices of mortgages only needed to have enough assets on hand to convince their trading partners that they would be solvent in the near term. Second, house prices went up so far so fast that they came crashing down much faster than anyone thought possible, wreaking havoc on everyone's risk models. The net result is that, among the institutions who were active in the market for packaged debt, nobody's sure that anyone else has enough assets to cover their obligations, or that they'll have enough assets tomorrow. Confidence is gone, and nobody is willing to do business with anyone else. How Will $700 Billion Help? The fly in the ointment is setting a price at which the government will buy these distressed securities. If the government (that is, you and me as taxpayers) pays too much, then it takes a loss and winds up subsidizing a bunch of money-grubbing hedge funds. Pay too little and the taxpayers make a profit (which is the American Way after all), but the seller may go bankrupt anyway. I'm actually not too worried about the government paying too little: presumably nobody is going to be forced to sell us these toxic assets, so they have the option of walkng away if the price is too low. If a few banks and hedge funds go bankrupt despite unloading their bad holdings, then they almost certainly would have gone under anyway. We're no worse off in that scenario, and maybe a little better since at least the dregs of the bankrupt firm will be easy to value. Won't This Cause Inflation? I'm not as worried about inflation on further reflection. One of the big effects of the housing bubble was to create vast amounts of wealth from thin air as home prices went up, and many people spent a lot of that wealth through cash-out refinancing. Now that housing prices are dropping and investors are deleveraging (reducing the ratio of debt to assets), huge amounts of money are being sucked out of the economy. This $700 billion bailout will serve to replace some of the money which is being vaporized through deleveraging and declining asset prices. It's also worth pointing out that the government isn't going to just hand out dollar bills. We will get assets in return, in the form of these mortgage-backed securities, and at a discount. As the underlying mortgages are paid off, the government gets to pay off whatever money it borrowed to facilitate the bailout in the first place. If we play our cards right, there might even be a small profit. Who Are the Winners and Losers?

Posted at 07:35 PM | Permalink | Sunday - September 07, 2008 03:05 PMPredictable ResultsOne of the crabapple trees outside our home has a wasp's nest the size of a basketball in it. Yesterday Scooter and Skeeter thought it would be great fun to start throwing stuff at it. The results were predictable, and Scooter has a nice sting which has swollen his left eye almost shut. He insists it was his younger brother bothering the wasps, but one of the bricks I found on the ground could only have been thrown by Scooter. No matter. Natural consequences are a Good Thing, we now know that Scooter isn't allergic to wasp stings, and maybe next time they'll know to leave the little meanies alone. Some fights just aren't worth picking. According to a couple of web sites, wasps get very sluggish and have a hard time flying when the temperature is below 50 degrees. Fortunately we're going through some cool weather now, and the overnight low is forecast to be 47. First thing tomorrow I'll finish the cleanup. Posted at 03:05 PM | Permalink | Wednesday - August 13, 2008 02:38 PMI have no energy!I just discovered that in my transition to the new version of iBlog, my entire "Energy" category disappeared. It looks like the only way to get it back is to recover the entries by hand, a task I'm not likely to complete for a while. In the meanwhile, here is a link to the old energy category page. Posted at 02:38 PM | Permalink | Thursday - August 07, 2008 03:30 PMTesting....testing...I was forced to upgrade to iBlog 2.0 (beta) a few weeks ago, and unfortunately it broke all my site templates. I think I have everything fixed now, but please bear with me if you notice any oddities. Posted at 03:30 PM | Permalink | Saturday - June 21, 2008 10:51 AMObama Fat Cats

I've been supporting Obama for President for several months now, and now that he's decided to give up public funding for his campaign he's going to need a lot of help from the "fat cats," big donors with deep pockets willing to give lots of money.

Who are these "fat cats," and how can we identify them? For the Obama campaign, the average donation is in the neighborhood of $150. Given that, I think anyone who gives $250 or more to the Obama campaign qualifies as a "fat cat." In order to identify these people I'm going to give an "Obama Fat Cat" car magnet to anyone who has given over $250 to the Obama campaign. Why? Because it's important to get out the message that this is a campaign with tens of thousands of "fat cats," not just the usual bunch of highly connected donors. I don't have a design yet, but I was thinking of something cute and cartoony (suggestions are welcome--leave them in the comments). If you've given $250 to Obama's campaign, send me an e-mail with your name and address to , and I'll mail you a magnet when I have them ready (I reserve the right to verify your fat cat status against one of the Internet databases of campaign donors). This is something I'm doing totally on my own, and I don't have any connection to the Obama campaign other than some of my own dollars going to their coffers. Please pass this around. The more fat cats the better! Posted at 10:51 AM | Permalink | Sunday - June 15, 2008 02:23 PMSan Francisco Scuba Map, circa 2050

Climate Change Skeptic: "I don't see what the big deal is. The Earth's atmosphere has had CO2 levels this high in the past."

Climate Change Believer: "Yes, but the last time that happened, sea level was 300 feet higher than it is today."

I'm not sure where I heard that exchange, and I'm not sure if it's true, but it inspired me to perform an interesting thought experiment: what would be underwater if the sea level rose 300 feet?  All of Florida and much of the southeast United States would become a shallow sea. The Mississippi would empty into the Gulf of Mexico somewhere around the confluence with the Ohio River at the southern tip of Illinois. And San Francisco? It would look something like the map I made (click on the thumbnail for a full-size version). To produce this Map of San Francisco Under 300 Feet of Water, I downloaded a 7.5 minute topographic map from the U.S. Geologic Survey, then traced around the 300 foot contour in Photoshop. I left the water slightly transparent so you can see the layout of the submerged streets and other features. Here in Minnesota we would have nothing to worry about--except for all the people moving in to enjoy our newly moderate climate, thanks to the improved proximity to the Gulf of Mexico (hurricanes might become an issue, too). All of Minnesota is well above 300 feet in elevation. As much fun as it was to make the Scuba Map of San Francisco, 300 feet of sea level rise is close to an impossible scenario. Even if all the ice caps (Antarctica and Greenland) completely melted, sea level would only rise around 200 feet--and no scientists I know of think that complete melting the Antarctic ice sheet is anything close to a realistic possibility. A more likely outcome of global warming is a sea level rise of a foot or two over the next century--devastating enough, to be sure, but not nearly as much fun to put on a map of San Francisco. Posted at 02:23 PM | Permalink | Sunday - June 15, 2008 12:37 PMBlogging drought, rainfall glut

It's been almost two months since I've updated this blog. Part of that was due to a technical issue: for some reason my hosting provider decided to block my home IP address. My guess is that my regular update of the "current weather" page (runs automatically every 15 minutes) looked like a robot attack to some automated script somewhere. Anyway, it took me several weeks to get around to debugging the problem and figuring out which tech support to complain to. It's working now.

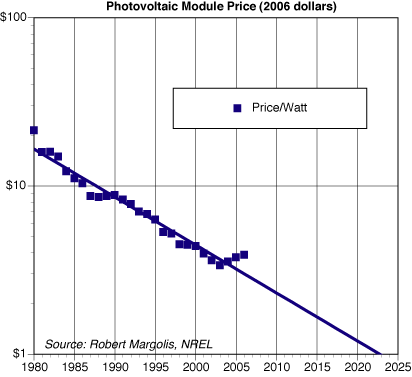

The other reason for the hiatus is the weather. Now that we're having some beautiful late spring/early summer weather (ignoring the fact that cities are underwater just a couple hundred miles south of here), I've been spending a lot of time working in the yard. So far I've replaced a hedge, finished about half of a retaining wall project, and spread four truckloads of wood chips. I've also recently acquired a recumbent tricycle for commuting, with the intent of cutting way back on my car usage. Depending on the price of gas and how much I can realistically offset, I can probably pay for it in a few years (total gasoline savings so far: $1.98). More on that later.... Posted at 12:37 PM | Permalink | Sunday - April 27, 2008 02:49 PMThe Magic YearIt's always dangerous to extrapolate current trends far into the future, but I've been doing it anyway for solar energy. I got my hands on a data set of the average price of photovoltaic modules over the past 25+ years (in constant 2006 dollars), thanks to Robert Margolis at NREL. Keeping in mind that the data shows the prices of the PV modules only (not installation), the trend is remarkable: on average, the real price per watt of photovoltaic modules over the past 25 years has tracked almost perfectly to a curve which drops by half every 10.5 years (or about 6% per year). There are a few blips here and there--corresponding to supply and demand fluctuations--but the simple 6% annual drop in prices explains 96% of the variation in PV module cost over two and a half decades.

Given recent advances in photovoltaic technology, there's no reason to believe the trend won't continue for a while longer. It may even accelerate at some point. At this point, it's natural to ask when solar panels will be cheaper than power from the electric company. You have to make some assumptions about the long term interest rate, how long the modules will last, and the relative cost of installation, and I came up with the answer that solar and grid power will be at parity somewhere between 2020 and 2025. That's not the whole story, though, since it's reasonable to assume that the cost of electricity will increase faster than inflation for the foreseeable future. That means that while the cost of solar power is going down every year, the savings will go up--and the savings will continue to increase even after the solar panels are bought and paid for. So in reality, it makes financial sense to install a photovoltaic system while it's still somewhat more expensive than grid power, since over the life of the system the savings will continue to increase. The Magic Year--the year when a brand-new photovoltaic system will pay for itself over its lifetime--depends on the assumptions you use about the inflation rate for electricity, the real interest rate, the life of the system, and so forth. The Magic Year is 2015

I used a Net Present Value (NPV) calculation, the standard way to figure the current value of future cash flow or savings. If the NPV is negative, then the system costs more to install than it saves over its lifetime; conversely, a positive NPV means the system pays for itself. The breakeven point (NPV = 0) is the Magic Year. Your Magic Year may be different than mine. For example, in the California desert where grid power is more expensive and a photovoltaic system produces more power over a year, the Magic Year could be as early as 2007 (using the same interest rate and inflation assumptions). In Seattle, where hydro power is still cheap and it's cloudy all the time, the Magic Year could be 2025 or later. Saving for the Magic Year In the meanwhile, we'll keep burning firewood in the winter--the stove has now paid for itself with gas savings--and doing smaller energy upgrades along the way like windows and lighting. 2015 is only seven years away, and by then we hope to have our net home energy use down to zero. Posted at 02:49 PM | Permalink | Monday - April 07, 2008 02:10 PMInscribed on Charlton Heston's Tombstone"Okay, you can take my gun now." Posted at 02:10 PM | Permalink | Tuesday - March 11, 2008 05:05 PM50! *

Spring is finally here--after months of nearly-continuous days below freezing, the temperature shot up to 50 degrees today. Thank the intense sunlight (we're now getting as much sun each day as we did at the end of September) and favorable westerly winds.

To be precise, our home weather station recorded a high of 49.7, which while it isn't precisely 50, it is close enough if you round to the nearest degree. Hence the asterisk. When it's 50 outside and bright sunshine, the house stays at a comfortable temperature all by itself: I let the stove go out, despite the fact that I'm home this afternoon (with a cold). I can practically see the snow disappearing before my eyes, and the highs are forecast to stay above 40 for pretty much the rest of the week. By this weekend, the snow cover which has persisted since early December may be completely gone. I love all the seasons in Minnesota, but Spring is easily my favorite, followed closely by Fall. I love those moments when we pass through Perfect while going from one extreme to the other. Posted at 05:05 PM | Permalink | Thursday - March 06, 2008 09:20 AMBlood in the water on Wall StreetThe stock market opened down big this morning (30 minutes into trading, the S&P 500 is down well over 1% with no bottom in sight). The news in the Wall Street Journal is alarming: the private equity fund Carlyle Capital failed to meet a margin call last night. A margin call is the second worst thing which can happen to any investor. It means that the investor borrowed money against its portfolio, and the bank or brokerage is demanding more collateral for the loan because the value of the portfolio dropped too much. The usual response is to add more cash to pump up the portfolio value and reduce the loan amount. Normally when an investor gets a margin call, there's only a matter of hours to put up enough collateral (or "meet the margin call"). If the problem isn't fixed by the start of trading the next day, the bank or broker will force the investor to start selling part of the portfolio to pay back enough of the loan to satisfy the collateral requirements. This forced selling is the worst thing which can happen to an investor. That a private equity fund as prominent as Carlyle Group would fail to meet a margin call is nothing short of astonishing. Aside from the fact that they should have been smarter than to get themselves in this situation in the first place, this was the group all the conspiracy nuts liked to weave their dark theories around, because of the number of prominent politicians (including ex-Presidents) associated with the fund. There's an old saying among stock traders that you should buy when there's blood in the water. In other words, when a big player is wounded or dying, the forced selling will push prices to an irrational place and that's the time to step in and buy. This morning there's blood in the water. Too bad I'm already invested. Posted at 09:20 AM | Permalink | Friday - February 22, 2008 11:07 AMEconomic outlook

The majority of pundits lately have been thinking deeply about the economy, at least when they're not obsessed with the scandal du jour in the presidential contest.

I'm not a pundit, but I occasionally pretend to be one on the Internet, and I've been thinking about the economy lately. Here's my conclusions: First, we are probably in a recession. When the dust settles, we'll probably decide that the recession began sometime between November and January. Second, I think we're probably close to the bottom right now (but we won't know that for a good six months or more). I base this on these observations: 1) The stock market has been basically flat for a month now, neither moving significantly up or down. We may have actually set the bottom in January, though we haven't moved enough up to be sure that there won't be another bottom in the near future. 2) The Fed is pumping huge amounts of liquidity into the economy, and that money is going to have to go somewhere. Near-term it seems to be going into super-safe investments like government bonds (and especially inflation-protected bonds), but before long investors will start looking for more return, and that means investing money in real businesses and people. 3) Media reports are uniformly and overwhelmingly focused on the negative, and not the positive news--and there is positive news out there, it's just hard to find. I take this as a sign that the mood can't get much worse from here. Third, just as in the past couple economic slowdowns, all the money the Fed is pumping into the economy right now is likely to lead to a new bubble somewhere in a couple years. Don't believe me? Look at the pattern: the 1992 recession was arrested by easy money from the Fed, which contributed to the dot-com bubble. The 2002 recession was also marked by easy money from the Fed, and that helped pump up the real estate bubble. This isn't necessarily a bad thing. Financial bubbles (despite the problems when they burst) have a number of desirable side-effects, not the least of which is driving a period of strong economic growth. Bubbles also tend to create massive investment in infrastructure which--even if uneconomical when built--lay the groundwork for future innovations and benefits. For example, a massive amount of fiber-optic capacity was built in the late 90's, far more than would be needed at the time. But the telecoms which lost their shirts on that fiber also created the conditions for cheap bandwidth today and made companies like YouTube possible. For the most part, the excess housing built this decade won't disappear, and (as long as the population continues to grow) there will be families willing to buy or rent the homes for the right price. What's The New Bubble? If you think there's going to be a new financial bubble forming in the next few years, it's very useful to know where the bubble might form. Good candidates are industries or sectors where: 1) Fundamentals have changed significantly for the better recently, and are likely to remain favorable. This could be due to new technology, market conditions, or other circumstances. 2) Returns have been good. 3) There's an element of sexiness or the exotic to pique investors' interest. The most obvious place is alternative energy: if you believe that oil is likely to remain around $100/barrel or higher for the indefinite future--and this seems a reasonable assumption--then the fundamentals for renewable energy are strong. Combine that with improving technology and dropping prices for renewable sources like wind and solar, and the sexiness of "green energy," and it looks almost irresistible. What's more, if you believe that renewable energy will ultimately have to replace nearly all our fossil fuel consumption, there's enough demand for renewables to sustain industry-wide growth of 25% to 50% per year for decades. First Draft of a Renewable Energy Portfolio To test this investment thesis, I took a stab at building a model portfolio over the weekend. I started with a comprehensive list of alternative-energy related companies (which was hundreds) and applied these criteria: 1) The stock has to be listed on the NYSE or NASDAQ. No pink sheet stocks or bulletin board stocks; any company with serious prospects will have the resources to get listed on a "real" exchange. Also, no foreign exchanges, since those are harder for Americans to buy, and I'm not familiar with the foreign accounting and trading rules. 2) The company has to be primarily focused on alternative energy. This excludes companies like GE, which makes a lot of wind turbines, but makes most of its money elsewhere. 3) No biofuels, because I'm not convinced that biofuels make economic or environmental sense in the absence of government supports. This left me with 14 companies, all but one of which make solar panels (the other company is a tiny manufacturer of wave power systems). Also, because this is a hyper-growth industry, I weighted the model portfolio by revenue growth in dollars from 2006 to 2007. That eliminated two companies which actually shrank (one due to an accounting change which I didn't want to bother researching). I also applied a cap of 15% of the portfolio value to individual companies, to keep it from being too heavily weighted towards a couple big Chinese companies. Of the twelve remaining companies, about 60% of the portfolio wound up in four big Chinese manufacturers of conventional (polysilicon) solar panels, and First Solar, the upstart thin film manufacturer, was another 13.5%. Unfortunately, this has been a really bad week for my model solar portfolio: all but two of the companies are down for the week, and the portfolio as a whole is down 15%. Apparently one of the big Chinese companies lowered its forecasts because of cost and availability problems with polysilicon, and that pulled down the entire industry (even the companies not using polysilicon). Volatility is to be expected in this sort of concentrated, speculative portfolio, but I'm really glad I didn't invest any actual dollars in it this week. Posted at 11:07 AM | Permalink | Friday - February 22, 2008 10:08 AMTen Business Lessons

Rob at Businesspundit is signing off today, and he ends with a list of ten lessons he's learned about business after ten years of entrepreneurship.

I don't normally link to Businesspundit (mainly because he's loaded up the site with zillions of craptacular advertisements, widgets, and other blog-flotsam), but this article is excellent and worth reading for anyone thinking about starting a business. There's an eleventh lesson not mentioned, however: every entrepreneur will have to learn these lessons for himself. We're a stubborn lot by nature, and there's no substitute for getting burned a few times. Posted at 10:08 AM | Permalink | Sunday - February 03, 2008 11:29 AMReally Frozen North

2007-2008 is the first Real Winter(tm) we've gotten in the Frozen North in a few years. A reasonable amount of snow, subzero temperatures, the whole nine yards.

Plus a new feature this year: the Temperature Roller Coaster. Most years, when we go into the deep freeze, we get a week or maybe ten days of consistently subzero temperatures, barely struggling into positive territory in the mid-afternoon if at all. This time around, we're getting short little bursts of bitterly cold temperature, followed by a warmup a day or two later, and then another plunge a few days to a week or two after that. This week was especially remarkable, as shown in the graph:  Over a 36-hour period, we went from +45 degrees to -15 degrees, a 60-degree swing. In the temperature plot you can almost see the exact minute the arctic cold front passed our house. The weather service likes to measure these things in nice 24-hour chunks, and on that basis this was apparently the biggest drop in decades. It was a little surreal to be walking around outside with no jacket on Monday, then all bundled up and worried about the car starting on Tuesday. Welcome to Minnesota. This week, they're forecasting a snowstorm on Monday, and more moderate temperatures (nothing below zero). We're past the midpoint of winter, there's noticeably more daylight now than back in late December, and it will get harder and harder for those arctic airmasses to compete against the warmer air coming from the Gulf of Mexico. We've also now completely consumed the five cords or so of firewood I'd stockpiled in the garage, so I'm now starting to move wood in from the outside piles. The wood in the garage lasted until February, almost exactly as long as I'd predicted. The supply is looking good, though I'm spending a fair amount of time picking through the piles to find the best wood to burn while it's still relatively cold out. The lighter wood (mostly cottonwood) is best for burning in the spring, when we don't need to keep the stove going all the time. It just burns too fast for the middle of winter. The biggest problem is that I've still got something like eight cords of cottonwood, most of it in large unsplit pieces. That's almost half a season's worth of wood, which is good, but there's so much of it that I'll be spending a lot of time splitting, stacking, and moving it. On the other hand, it was all free. Beggars can't be choosers. Posted at 11:29 AM | Permalink | |